Executive Summary

US e‑commerce sales have surged to over 16 to 17% of total retail (roughly $300 billion+ in Q1 2026), driven by consumers demanding fast, free and reliable shipping. Key data points: 45% of U.S. adults expect free shipping on any order, 90% will wait 2 to 3 days to avoid fees, and over 80% will still buy if delivery takes a week so long as it is free. Last-mile delivery has become a strategic driver of customer satisfaction, yet accounts for over 50% of total freight spend and remains a common point of failure.

Last-mile delivery is no longer just a logistics function. For many e-commerce brands, it has become a key customer experience touchpoint that directly influences loyalty, repeat purchases and brand perception. As customer expectations continue to rise, delivery performance increasingly impacts long-term business growth.

Retailers use a mix of models including in-house fleets, 3PLs, crowdsourced drivers, lockers, curbside pickup and hybrid networks, each balancing cost, speed and control. Technology enablers include route optimization, TMS/WMS, real-time tracking and emerging drone and robot solutions. Key metrics span cost per delivery, on-time rates, first-attempt success, delivery CSAT and CO₂ emissions. Route optimization alone can cut last-mile distance and emissions by up to 30%.

Market Context and Consumer Expectations

E‑commerce reached 16.9% of all U.S. retail sales in Q1 2026, reflecting steady 10%+ year-over-year growth. Analysts project mid single digit annual gains going forward as consumer behavior continues shifting.

Free and fast shipping is now expected as standard. A UPS study found 43% of consumers factor shipping costs into retailer choice; 90 to 95% prefer free shipping even with a 2 to 3 day delay; over 30% will shop elsewhere without it; and 73% choose one retailer over another based on same or next day availability. Cost sensitivity is extreme, with over 90% saying they will abandon a purchase if shipping costs are too high.

While delivery speed remains important, reliability has become an equally important factor in customer satisfaction. Many shoppers are willing to wait longer if delivery is free, predictable and arrives within the promised time window.

Expectations vary by segment: roughly 60% of Gen Z consumers will pay for same day delivery versus only 30% of Boomers. Rural shoppers tolerate delays in exchange for no fees, while urban customers rely heavily on home delivery. Over 80% of consumers say they will wait an extra day to consolidate deliveries into a single arrival.

Amazon Prime’s free 2 day (now 1 day) shipping set the industry standard, pushing competitors toward BOPIS and store based fulfillment. By 2020, 87% of major retailers offered buy online pickup in store or curbside pickup, up from 66% pre pandemic.

Economic headwinds are now cooling growth: inflation and tariffs have tempered spending, with AlixPartners (2025) reporting declining online purchases outside groceries. Simultaneously, 64% of large retailers experienced above normal carrier surcharges over the past two years, forcing brands to rethink last-mile strategy to protect margins.

Key Last-Mile Delivery Models

Retailers typically rely on six primary last-mile delivery models, each balancing cost, speed and operational control differently:

- In-House Fleet: Maximum control over customer experience, best suited for high-value, bulky or white-glove deliveries, but requires significant investment.

- 3PL Providers: Outsourced logistics and fulfillment that offer scalability and broad coverage while reducing operational complexity.

- Crowdsourced Delivery: Flexible, pay-per-use networks such as DoorDash, Uber and Instacart, ideal for same-day and on-demand delivery.

- BOPIS & Curbside Pickup: Customers collect orders themselves, reducing shipping costs and improving fulfillment speed.

- Parcel Lockers & Pickup Points: Consolidated delivery locations that lower costs and reduce failed delivery attempts.

- Hybrid Networks: A combination of carriers and delivery methods used to optimize cost, speed and service levels across different markets.

Comparison of Last-Mile Models: The table below summarizes these models by cost structure, control and suitability:

|

Delivery Model |

Cost Structure |

Brand Control |

Scalability |

Best For / Notes |

|

In-House Local Fleet |

High fixed (trucks, labor) |

Very High |

Hard to scale without density |

Premium service, large/bulky/fragile goods, scheduled delivery |

|

3PL Fulfillment & Carriers |

Variable, contract-based |

Moderate |

Strong if partner network is large |

Brands wanting outsourced scale and integration (e.g. warehousing + shipping) |

|

Crowdsourced (Gig) |

Pay-per-use (flexible) |

Low-Moderate |

Very fast in select markets |

On-demand/same-day in cities; small deliveries (food, consumer goods) |

|

Store Pickup / Curbside |

Low incremental (leverages stores) |

Moderate |

Scales with store footprint |

Grocery, big-box, returns – items customers can collect themselves |

|

Parcel Lockers / PUDO |

Low (bulk drop-offs) |

Moderate |

Strong where deployed (urban) |

Compact goods; reduces failed deliveries; customer convenience in cities |

|

Hybrid Multi-Carrier |

Mixed (optimized mix) |

Moderate-High |

Strong if managed centrally |

Multi-region brands; complex order profiles; balance cost vs. service |

Technology Enablers

Last-mile delivery typically accounts for 50 to 53% of total parcel shipping cost, with labor and fuel for low-density stops being the largest components. Every failed delivery attempt multiplies costs through redelivery, customer service and potential reshipping. Hidden costs extend far beyond transportation expenses. Late deliveries often generate customer support tickets, refunds, reshipments, negative reviews and lost future revenue. In many cases, the long-term impact on customer loyalty can exceed the direct shipping cost itself. Major carrier surcharges (fuel, residential and peak fees) have become additional margin drains in recent years.

Companies track the following KPIs:

- Cost per Delivery: Total last-mile cost divided by delivered orders. If this rises while sales grow, profitability is eroding.

- First-Attempt Success Rate: Percentage of orders delivered on the first try. As one logistics expert notes, “the best route is the one most likely to end in a completed delivery.”

- On-Time Delivery Rate: Share of orders arriving within the promised window, critical for narrow delivery commitments.

- Exception/Failure Rate: Tracks damage, address issues and no-shows, revealing operational weaknesses and correlating with high support load.

- Delivery CSAT: Post-delivery satisfaction score. Studies show 98% of consumers say delivery experience affects brand loyalty, and 84% will not buy again after a poor delivery. For many retailers, delivery satisfaction has become a leading indicator of retention and repeat purchase behavior, making it a strategic business metric rather than a simple operational KPI.

- Driver Productivity: Stops per route or packages per shift. Smart routing can increase stops per tour by up to 30%.

- CO₂ Emissions per Delivery: Last-mile accounts for up to 28% of transport emissions. Route optimization and fuller loads can cut distance and emissions by roughly 30%.

A well-rounded dashboard covers efficiency, completion, reliability, customer satisfaction and quality, enabling teams to link delivery performance directly to margin impact and churn risk.

Cost Drivers and Key Metrics

Modern last-mile relies on sophisticated technology at every step. Core enablers include:

Route Optimization and TMS: AI-powered routing software plans delivery sequences to minimize distance and time, integrating traffic data, vehicle constraints and delivery windows. Optimized routes reduce mileage by up to 30%, cutting fuel, labor and emissions. Transportation Management Systems (TMS) automate carrier selection, handing off orders to FedEx, UPS or local couriers based on geography and cost.

Warehouse and Inventory Systems (WMS/OMS): Modern e-commerce uses Warehouse Management Systems and Order Management Systems to speed pick/pack operations and enable micro-fulfillment through small urban warehouses. Amazon and Walmart integrate these systems with real-time inventory to split orders optimally between distribution centers and stores for faster delivery.

Real-Time Tracking and Telematics: GPS telematics provide constant delivery visibility, with carriers delivering live ETAs and notifications via apps or email. Approximately 50% of consumers now track shipments themselves. Sensors adding photo proof and cold chain temperature monitoring feed performance data to operational dashboards for both teams and customers.

Driver Mobile Apps: Apps for drivers and crowdsourced couriers provide optimized routes, real-time status updates and contactless proof of delivery. Platforms such as Bringg, FarEye and Salesforce Field Service are widely used. In-cab tablets further improve on-road safety and productivity.

Drones and Autonomous Vehicles: In 2025, Uber partnered with Flytrex for drone food delivery pilots, while Matternet launched commercial drone service in Los Angeles. Industry forecasts project 3 to 5 million drone deliveries per day by 2030. Sidewalk robots from Starship and Serve Robotics already handle short-range urban runs, with costs falling 20 to 30% annually. Autonomous vans and electric cargo bikes remain under active trial.

Electric Vehicles and Sustainability Tech: UPS, FedEx and Amazon are deploying thousands of EV delivery vans. Telematics monitor idling and fuel use, while software optimizes delivery consolidation by enabling customers to select preferred delivery windows, increasing fill rates and reducing total trips. Together these technologies address cost, consumer demand and sustainability pressures simultaneously.

Operational Challenges

Urban Congestion: Dense cities generate high delivery demand but bring traffic, limited parking and complex multi-unit buildings. These factors reduce first-attempt success rates and raise costs in metropolitan areas.

Rural Reach: Low order density across long distances makes next-day delivery infeasible and per-delivery costs high. USPS remains essential for universal rural coverage, as rural consumers still rely heavily on local stores.

Labor Shortage: The American Trucking Associations reported a shortage of roughly 78,000 drivers in 2022, with e-commerce fulfillment facing similar gaps. Holiday peaks intensify hiring difficulties, driving up wages and attrition.

Cost Volatility: Carrier rate hikes of up to 15%, volume caps and unpredictable fuel and residential surcharges complicate planning and force retailers into costlier secondary carrier arrangements.

High Return Rates: Approximately 20% of online purchases are returned versus 8% in-store. Reverse logistics adds cost and complexity, particularly in apparel and electronics, making efficient return management (curbside drop-offs, mail-back kits) an increasing operational priority.

Peak Demand: Holiday surges and major promotions overwhelm driver supply and carrier capacity, exposing weaknesses in any delivery model regardless of its sophistication.

Last-mile success requires balancing geography, density and demand. Going forward, logistics planners must adapt locally, investing in urban micro-warehouses and lockers while relying on stores and USPS for remote regions.

Vendor Landscape and Provider Comparison

A variety of carriers and solution providers compete and partner across U.S. last-mile delivery.

UPS and FedEx are the traditional national parcel carriers, offering extensive ground and air networks, next day and 2 day options, global reach and sophisticated tracking. Strengths include high reliability and integrated technology. Weaknesses include rising costs, peak volume limits and reduced agility in dense metro areas. FedEx continues to operate one of the largest parcel delivery networks in North America, offering both ground and express services across a broad geographic footprint.

USPS delivers to every U.S. address six days a week, with Ground Advantage often the cheapest option for light residential parcels and no fuel surcharge on First Class. Weaknesses include slower expedited service, limited tracking dashboards and occasional weekend reliability concerns.

Amazon Logistics (AMZL) comprises Amazon Flex, DSP partners and Amazon Air, enabling one day delivery within the Prime ecosystem. Its key limitation is availability: AMZL serves primarily Amazon orders, with third-party and non-Amazon coverage still limited compared to national carriers.

Regional Carriers such as LaserShip (Northeast), OnTrac (West Coast) and GSO/LSO (Southeast) offer lower prices and better on-time performance within their zones. Their weakness is limited geographic reach.

Courier Networks and Crowdsourced Platforms including Roadie, DoorDash, Instacart and Uber Eats provide same day delivery by tapping large gig driver pools. Strengths include speed and consumer app reach. Weaknesses include limited product categories and variable service quality.

3PL Fulfillment Services such as ShipBob, Deliverr and Rakuten Super Logistics offer end-to-end fulfillment with multi-carrier integration and e-commerce platform connectivity. Weaknesses include reduced brand control, complex tiered pricing and potential capacity constraints.

Parcel Lockers and Retail Networks including Amazon Hub, UPS Access Point, FedEx Office and InPost provide customer pickup alternatives, serving as important last-mile nodes that reduce failed deliveries without requiring direct carrier involvement.

Below is a comparison table summarizing strengths and weaknesses of major provider categories:

|

Provider(s) / Network |

Model Type |

Strengths |

Weaknesses |

|

UPS, FedEx (National) |

Parcel Carrier (3PL) |

Nationwide network, fast options (overnight/2-day), strong tracking and reliability. |

Higher rates/surcharges; peak volume caps; less flexible in hyperlocal delivery. |

|

USPS (Postal Service) |

Postal Network |

Delivers to all addresses (broadest reach), cost-effective for small/light packages, no fuel surcharges. |

Limited tech integration, slower for express shipments, weekend and evening coverage limited. |

|

Amazon Logistics (AMZL) |

In-house e-commerce |

Super-fast to Prime members, integrated with Amazon platform, subsidized shipping costs. |

Only handles Amazon-originated orders (limited to platform); dependent on Amazon’s fulfillment footprint. |

|

Regional Carriers (OnTrac, LaserShip) |

Regional Ground |

Cheaper than nationals in coverage area, flexible capacity (partner networks). |

Fragmented coverage; inconsistent performance outside core zones; often focus on high-volume areas. |

|

Crowdsourced (DoorDash, Instacart, Uber) |

Gig Delivery |

Rapid same-day in urban areas, easy to deploy (no driver hiring), known user apps. |

Variable quality; largely for perishable/retail goods, not bulk; less branded control, service guarantees. |

|

Fulfillment 3PLs (ShipBob, Deliverr) |

Integrated Fulfillment |

All-in-one warehousing + shipping, tech integration (OMS/WMS), multi-carrier choice. |

Higher fees (fulfillment + shipping); less transparent for small brands; added layer between brand and delivery execution. |

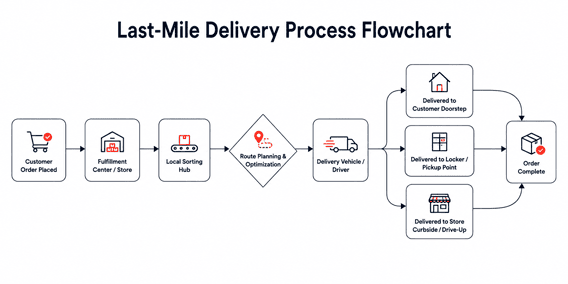

Last-Mile Delivery Process Flowchart

The typical last-mile workflow (from order to delivery) can be summarized as follows:

Case Examples

Retail Partnerships with Gig Platforms: Retailers including Kohl’s, Lowe’s and Petco have partnered with DoorDash, Instacart and Uber for same-day delivery. Approximately 29% of retailers now use crowdsourced networks, citing flexible scale and easy startup. Integrations typically run via API, with gig drivers picking up orders directly from stores or micro-warehouses.

Store Fulfillment at Scale: Walmart, Target and Home Depot have aggressively expanded BOPIS and curbside pickup. Walmart reported 8 to 10 times growth in store pickup during 2020, allowing customers to collect orders within hours while bypassing carrier caps. Walmart, Target and major grocers now connect online inventory with in-store picks, often integrating Instacart or Shipt.

Amazon’s Last-Mile Buildout: Amazon Flex and Delivery Service Partners cover most U.S. metros for Prime delivery. Prime Air drone pilots and autonomous van testing point to future investment, while tens of thousands of Amazon Hub locker locations nationwide offer consumers alternatives to home delivery.

Future Trends

Autonomous and Robotic Delivery: Drones could make millions of daily deliveries by 2030. Wing, Flytrex, Matternet and Amazon are pursuing UAV approvals, while Serve Robotics and Starship are scaling sidewalk bots for groceries and meals. Combined drone-robot handoff systems will extend range.

Electrification and Sustainable Fleets: UPS committed to 10,000 EVs by 2026, with FedEx and Amazon pursuing similar targets. As low-emission zones expand across U.S. cities, EVs and eventually hydrogen fuel cells will become standard, supported by software optimizing charging schedules.

Micro-Fulfillment Centers: Urban dark stores and micro-fulfillment hubs in retrofitted retail or container spaces enable one-hour and same-day delivery. Early pilots show 30 to 50% faster fulfillment, with deeper integration between micro-fulfillment and order management systems ahead.

Data and AI: Machine learning will drive predictive inventory placement, dynamic carrier allocation and smarter delivery promises such as two-hour windows offered only when operationally feasible. Continuous learning in route planning will become standard. AI will also help retailers proactively identify delivery risks, forecast demand spikes and optimize inventory positioning before disruptions impact customers.

Sustainability and Regulation: Local governments may mandate zero-emission fleets and tax inefficient small-shipment practices to encourage consolidation. Tax credits for EVs and shared locker infrastructure will expand as offsetting incentives.

Consumer-Driven Innovation: Growing consumer willingness to accept slower consolidated shipping will enable new models such as subscription delivery guarantees (Walmart+, Amazon Prime) and discounted carbon-neutral delivery windows as a service.

Resilience and Network Reshoring: Supply chain disruptions are pushing brands toward regional last-mile footprints, smaller local distribution centers and competitor inventory pooling. Locker networks and store partnerships provide backup channels when traditional carriers face peak overload.

Summary: U.S. last-mile is rapidly evolving toward multi-modal, data-driven delivery combining drones, robots, EVs and pickup lockers. Winning strategies will balance customer-centric delivery promises with cost discipline, adapting models to local density, product type and geography while keeping sustainability requirements at the center of decision-making.